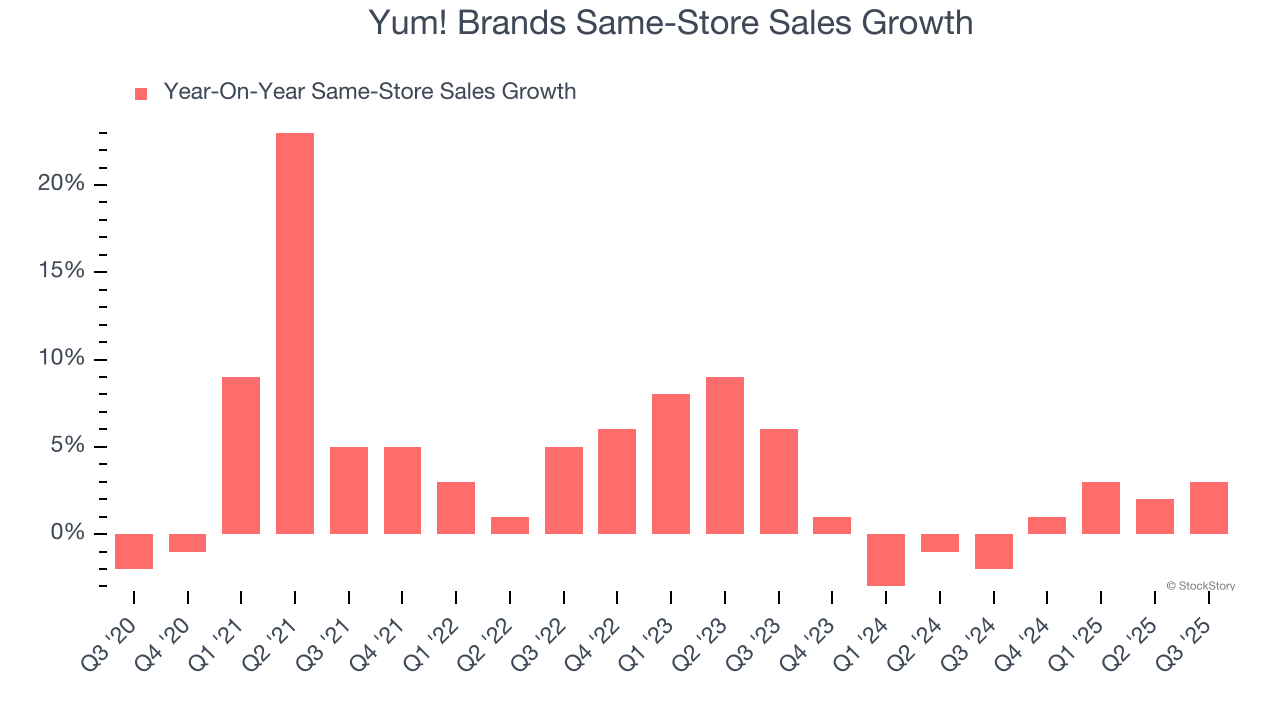

Yum Brands didn’t just meet Wall Street’s expectations—it left them in the dust. The parent company of Taco Bell, KFC, and Pizza Hut posted earnings that topped estimates, powered by an impressive 8% same-store sales increase at Taco Bell. This wasn’t a fluke or a one-off quarter of momentum. It was the result of disciplined menu innovation, digital transformation, and a deep understanding of shifting consumer behavior in the quick-service restaurant (QSR) space.

The broader market has been cautious about consumer spending amid inflationary pressures and mixed economic signals. Yet Yum Brands delivered, proving that brand strength, operational efficiency, and targeted growth strategies can cut through uncertainty. At the center of this success? Taco Bell, which continues to outperform not just within the Yum portfolio but across the entire QSR landscape.

Taco Bell’s 8% Growth: Fueling Yum’s Momentum

Taco Bell’s 8% same-store sales growth wasn't driven by a single tactic but by a layered approach that resonated with cost-conscious yet experience-driven consumers. The brand leaned heavily into value messaging without devaluing its offerings—premium items like the Crave Case and layered menu bundles gave customers perceived savings while boosting average ticket sizes.

More importantly, Taco Bell doubled down on digital. Mobile ordering, loyalty program expansion, and app-exclusive deals created a feedback loop: more engagement led to more data, which in turn fueled hyper-personalized promotions. That digital engine accounted for over 30% of Taco Bell’s U.S. sales in the quarter—a number that reflects both infrastructure investment and behavioral shift.

Consider this: a limited-time offering like the Quesalupa or the return of fan favorites like the Mexican Pizza didn’t just stir social buzz—they were amplified through targeted app notifications and geo-fenced promotions. The result? Sustained traffic and meaningful lift in same-store figures, not just short-term spikes.

How Same-Store Sales Translate to Real Earnings

Same-store sales (SSS) growth is one of the most telling metrics in retail and restaurant earnings. It measures revenue from existing locations, stripping out the noise of new store openings. An 8% SSS increase at Taco Bell means customers aren’t just visiting—they’re spending more, more often.

For Yum Brands, this translated directly into bottom-line performance. The company reported adjusted earnings per share (EPS) of $1.38, beating the consensus estimate of $1.29. Revenue climbed 7% year-over-year, with the U.S. segment—where Taco Bell dominates—showing the strongest gains.

But it’s not just about the numbers. The quality of the growth matters. Unlike growth fueled by discounting or temporary promotions, Taco Bell’s increase came with stable margins. That suggests pricing power and operational discipline, not just volume.

Key Drivers Behind the SSS Growth: - Menu innovation: Limited-time offers (LTOs) that create urgency without cannibalizing core sales. - Value tiers: Multi-price-point bundles (e.g., $5 Crave Case) that appeal across income segments. - Digital adoption: App-based loyalty program now boasts over 40 million members. - Operational efficiency: Improved drive-thru speeds and kitchen throughput.

Yum’s Portfolio in Focus: Why Taco Bell Outshines KFC and Pizza Hut

While Taco Bell surged, KFC and Pizza Hut delivered more modest results. KFC posted a 4% same-store sales increase in the U.S., solid but unspectacular. Pizza Hut, meanwhile, saw flat U.S. same-store sales despite international growth, particularly in emerging markets.

This divergence highlights a strategic truth: not all QSRs are evolving at the same pace. Taco Bell has positioned itself as a youthful, agile brand, embracing digital culture, TikTok trends, and Gen Z preferences. Pizza Hut, despite attempts to rebrand around delivery and wings, still battles perceptions of being outdated. KFC, while strong globally, hasn’t matched Taco Bell’s momentum in the U.S. market.

| Brand | U.S. Same-Store Sales Growth | Digital Mix | Key Challenge |

|---|---|---|---|

| Taco Bell | 8% | 32% | Maintaining innovation velocity |

| KFC | 4% | 22% | U.S. brand relevance |

| Pizza Hut | 0% | 40% | Menu differentiation |

Taco Bell isn’t just leading Yum’s portfolio—it’s setting the tone. The brand’s ability to launch culturally relevant campaigns (like its “Live Más” ethos) while maintaining cost efficiency gives it a rare dual advantage: emotional connection and economic sense.

The Role of International Markets in Yum’s Earnings

While Taco Bell drove U.S. performance, Yum’s international business remains a critical engine. The company operates over 55,000 restaurants in more than 150 countries, with KFC particularly strong in China and India.

In China, Yum China—a separate publicly traded entity—reported strong recovery as post-pandemic dining demand rebounded. But globally, same-store sales for KFC rose 6%, benefiting from pricing and new store formats in Southeast Asia and the Middle East.

Pizza Hut’s international division saw 5% growth, driven by expansion in Africa and the Caribbean. These markets offer long-term potential, but they’re not moving the needle like Taco Bell’s U.S. performance. The takeaway? Domestic strength—specifically Taco Bell’s resurgence—was the primary catalyst behind Yum Brands’ earnings beat.

Still, international diversification provides insulation. When U.S. inflation pressures wages or supply chains, emerging markets with lower labor costs and growing middle classes offer counterbalance. Yum’s franchise-heavy model amplifies this: over 99% of its locations are franchised, limiting capital risk while collecting steady royalty streams.

Strategic Moves Behind the Scenes

Yum’s success isn’t accidental. Over the past three years, the company has made calculated investments that are now paying off:

- Digital infrastructure: A $150 million investment in tech platforms improved app functionality, data analytics, and supply chain visibility.

- Franchisee support: Training programs and co-op marketing funds helped franchisees execute national campaigns locally.

- Menu rationalization: Removing underperforming items increased kitchen efficiency and reduced waste.

- Delivery optimization: Partnerships with DoorDash, Uber Eats, and in-house delivery models improved speed and consistency.

One often-overlooked factor: Yum’s supply chain resilience. While competitors faced shortages, Yum leveraged centralized procurement and regional hubs to maintain ingredient availability. This operational backbone ensured that when demand spiked—say, during a viral TikTok trend—the supply could keep up.

Franchisees benefit, too. With stable supply and strong brand momentum, they’re more willing to invest in reimaging older locations or testing new formats like Taco Bell Cantinas—upscale versions with full bars and enhanced interiors.

Investor Reaction and Market Implications

Wall Street responded swiftly. Shares of Yum Brands rose over 6% in after-hours trading following the earnings release. Analysts upgraded targets, citing not only the immediate beat but the sustainability of Taco Bell’s growth model.

More telling was the shift in sentiment. For years, investors questioned whether Taco Bell had peaked. Could a brand built on affordability and convenience evolve without alienating its core audience? This quarter answered with a resounding yes.

But caution remains. Labor costs are still elevated. Commodity prices, especially for beef and cheese, could squeeze margins if not managed. And competition is intensifying—Chipotle, Wendy’s, and even McDonald’s are sharpening their value plays.

Still, Yum’s ability to outperform in this environment signals durability. The company now trades at a premium to its historical average, reflecting confidence in its trajectory. As long as Taco Bell keeps innovating and the broader portfolio stabilizes, that premium may be justified.

What This Means for the Future of QSR

Taco Bell’s 8% growth isn’t just a win for Yum—it’s a blueprint for the modern QSR. The era of relying solely on foot traffic or TV ads is over. Today’s winners blend digital fluency with cultural relevance and operational rigor.

Other chains are taking notes. Wendy’s is expanding its loyalty program. McDonald’s is testing AI-driven drive-thrus. But Taco Bell’s advantage lies in agility. It can launch, test, and scale ideas faster than larger, more bureaucratic competitors.

For franchisees and investors, the lesson is clear: invest in digital, listen to your customer base, and don’t fear bold innovation—even if it means redefining what your brand stands for.

Closing: How to Leverage Yum’s Playbook

Yum Brands’ earnings beat, driven by Taco Bell’s 8% same-store sales growth, is more than a quarterly headline—it’s a masterclass in modern restaurant strategy. The takeaway isn’t just that value sells, but that value combined with experience, speed, and personalization creates lasting momentum.

For brands looking to replicate this success, the path is clear: - Prioritize digital engagement as a core channel, not an add-on. - Use data to tailor promotions and menu offerings. - Empower franchisees with tools and support. - Innovate rapidly, but keep the core menu strong. - Monitor costs without sacrificing quality.

Taco Bell didn’t win by being the cheapest. It won by being relevant, responsive, and relentlessly customer-focused. In a market where attention is scarce and spending is scrutinized, that’s the recipe for staying on top.

FAQ

What caused Taco Bell’s 8% same-store sales growth? A mix of successful limited-time offers, digital engagement, value bundling, and improved operational speed drove increased customer visits and higher average checks.

How did Yum Brands’ earnings compare to estimates? Yum Brands reported adjusted EPS of $1.38, beating the consensus estimate of $1.29, with revenue up 7% year-over-year.

Why is same-store sales growth important? It reflects performance at existing locations, indicating real demand rather than growth from opening new stores.

How does Taco Bell’s digital strategy differ from competitors? Taco Bell integrates its app deeply with loyalty rewards, personalized offers, and social media trends, creating a closed-loop engagement system.

What challenges does Yum Brands still face? Persistent inflation, labor costs, and uneven performance at Pizza Hut and KFC in the U.S. pose ongoing risks.

Is Taco Bell’s growth sustainable? Yes, if the brand continues innovating, maintains supply chain stability, and adapts to evolving consumer habits.

How much of Taco Bell’s sales come from digital channels? Over 30% of U.S. sales are now digital, with app-based orders and loyalty members driving repeat business.

FAQ

What should you look for in Yum Brands Earnings Beat Forecasts on Taco Bell’s 8% Sales Surge? Focus on relevance, practical value, and how well the solution matches real user intent.

Is Yum Brands Earnings Beat Forecasts on Taco Bell’s 8% Sales Surge suitable for beginners? That depends on the workflow, but a clear step-by-step approach usually makes it easier to start.

How do you compare options around Yum Brands Earnings Beat Forecasts on Taco Bell’s 8% Sales Surge? Compare features, trust signals, limitations, pricing, and ease of implementation.

What mistakes should you avoid? Avoid generic choices, weak validation, and decisions based only on marketing claims.

What is the next best step? Shortlist the most relevant options, validate them quickly, and refine from real-world results.